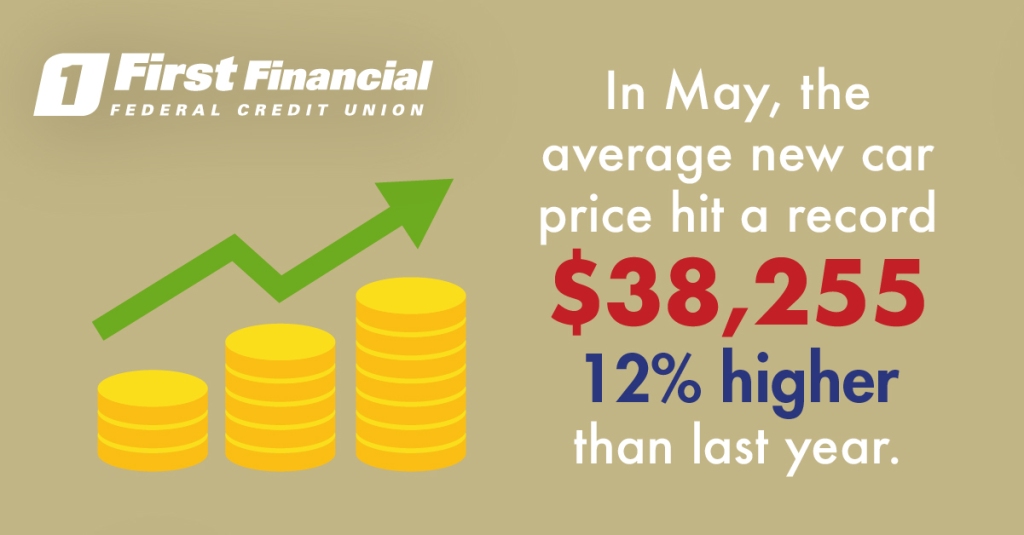

The average new car price hit a record high of $38,255 last month, according to JD Power. That’s up 12% from the same period a year ago.

If you’re out car shopping right now, be prepared to pay bigger bucks than usual for that vehicle. About two-thirds of car buyers paid within 5% of the sticker price last month, with some even paying above sticker price. That means there are fewer deals to be had and fewer negotiations taking place.

Why? Due to a computer chip shortage at auto plants around the world, car dealers are left with a fraction of the vehicles (both new and used) than what they typically have on hand. Since more people are buying used cars, they are also becoming as difficult to get as new cars.

Here are a few things to keep in mind if you’re in the market for a new or used vehicle right now:

- Don’t expect a great deal: Don’t be surprised if the dealership only discounts the vehicle you’re looking at by a few hundred dollars, if anything at all.

- Search outside of your community: Not finding what you want in your local area? Look at dealerships a bit further away from home. This can make a difference in getting the car you want or in hopefully getting a better deal.

- Ask for top dollar for your trade-in: One bright spot is if you have a vehicle to trade-in, because of the shortage – trade-in values are at an all-time high. This can help cushion the higher sales price.

- Hit pause: According to Edmunds, the vehicle shortages might last for another six months or so. If you’re not in a hurry to buy a car right now, their best advice is to wait a bit.

Are you still considering buying a new or used vehicle and need a loan? Click here to find out about a First Financial Auto Loan or get pre-approved to ensure you know where to start, what monthly payments you can afford and get the best deal possible for you.*

Waiting it out? You may be able to save by refinancing your current vehicle from another lender.** Click here to get started by filling out our online quick Auto Loan Review inquiry form.

Do you have a lease coming due soon? Another option is to keep the car you already know and love, by buying out your car lease.* Get started here.

*APR = Annual Percentage Rate. Not all applicants will qualify, subject to credit approval. Additional terms & conditions may apply. Actual rate may vary based on credit worthiness and term. A First Financial membership is required to obtain a First Financial auto loan and is available to anyone who lives, works, worships, volunteers or attends school in Monmouth or Ocean Counties. See credit union for details. A $5 deposit in a base savings account is required for credit union membership prior to opening any other account/loan.

**Not all applicants will qualify, subject to credit approval. First Financial FCU maintains the right to not extend credit, after you respond, if we determine you do not meet our guidelines for creditworthiness. Current loans financed with First Financial FCU are not eligible for review or refinance. A First Financial membership is required to obtain an auto loan and is available to anyone who lives, works, worships, volunteers or attends school in Monmouth or Ocean Counties. A $5 deposit in a Base Savings Account is required to establish membership.