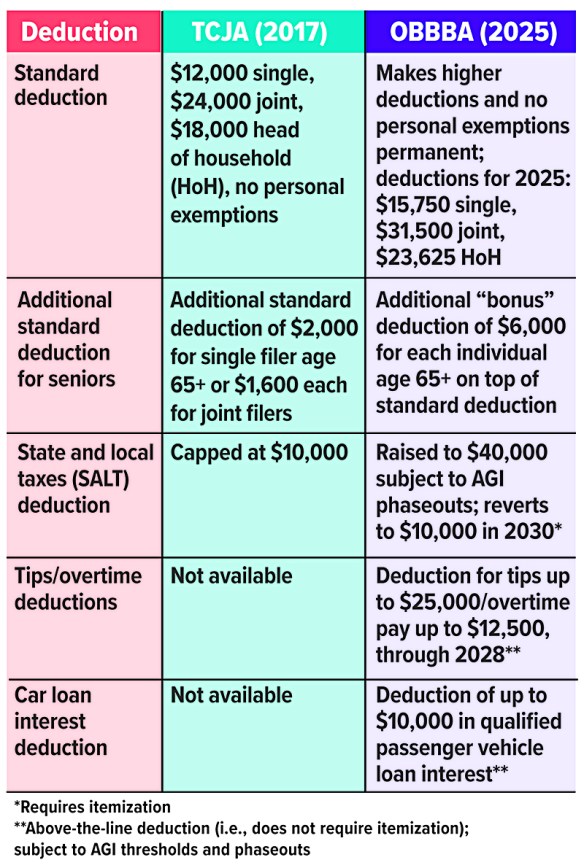

With the enactment of the One Big Beautiful Bill Act in July 2025, a new deduction for tips is effective for tax years 2025 through 2028. Here is a summary of the new provision and the occupations that will be affected.

With the enactment of the One Big Beautiful Bill Act in July 2025, a new deduction for tips is effective for tax years 2025 through 2028. Here is a summary of the new provision and the occupations that will be affected.

Deduction explained

Employees and self-employed individuals may deduct up to $25,000 per year of qualified tips, provided they work in an occupation the IRS views as “customarily and regularly” receiving tips on or before December 31, 2024. This deduction is available to taxpayers whether they claim the standard deduction or itemize.

Qualified tips include voluntary cash or card payments, whether given directly by customers or through tip sharing. Tips must be voluntary and do not include automatic gratuities and mandatory service charges. For self-employed individuals, the deduction cannot exceed their net income (before applying the deduction) from the business in which the tips were earned.

Eligibility details

- Taxpayers claiming the deduction must provide their Social Security number.

- Married couples must file jointly.

- Married couples filing separately are not eligible.

- Workers in excluded fields, such as health, performing arts, or athletics (and their employees), are ineligible.

- Employers must report tips and occupation details annually to the IRS or Social Security Administration and provide statements to workers.

- The total amount of qualified tips that can be deducted per calendar year is $25,000 regardless of filing status.

Deduction limitations

The deduction begins to phase out for single filers with Modified Adjusted Gross Income (MAGI) over $150,000 or over $300,000 for married couples filing jointly. The deduction is reduced by $100 for every $1,000 above these thresholds.

Qualifying jobs

In October 2025, the U.S. Department of the Treasury and the IRS published proposed rules listing the industries and occupations that qualify for the deduction, because tipping was customary and regular in these jobs before December 31, 2024. Here are the qualifying industries with some of the most common qualifying occupations.

- Beverage and food service: Bartenders, wait staff, baristas, bussers, cooks, dishwashers, hosts, and bakers

- Entertainment and events: Casino dealers, musicians, DJs, performers, ushers, ticket takers, and digital content creators

- Hospitality and guest services: Bellhops, concierges, hotel desk clerks, and housekeepers

- Home services: Cleaners, plumbers, electricians, landscapers, HVAC repair workers, and locksmiths

- Personal services: Nannies, babysitters, tutors, pet sitters, photographers, event planners, and personal caregivers

- Personal appearance and wellness: Hairdressers, barbers, massage therapists, nail technicians, estheticians, and tattoo artists

- Recreation and instruction: Golf caddies, tour guides, fitness instructors, self-enrichment teachers, and recreational pilots

- Transportation and delivery: Valets, taxi/rideshare drivers, shuttle drivers, delivery workers, charter boat staff, car detailers, and home movers

A detailed list of occupations can be found on the website of the Federal Register.

Workers in up to 68 occupations could see their tax burden reduced by the “no tax on tips” deduction.

IRS transition relief

For tax year 2025, the IRS will provide transition relief in the form of further guidance or additional time for qualified taxpayers and employers to adapt to the new reporting requirements.

The “no tax on tips” deduction will likely affect many tipped workers in the hospitality, food service, personal care, delivery, and other industries. Both taxpayers and employers should stay updated on all reporting changes and compliance requirements.

Questions about this topic? Contact First Financial’s Investment & Retirement Center by calling 732.312.1534. You can also email mary.laferriere@lpl.com or maureen.mcgreevy@lpl.com

Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker/dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. First Financial Federal Credit Union (FFFCU) and First Financial Investment & Retirement Center are not registered as a broker/dealer or investment advisor. Registered representatives of LPL offer products and services using First Financial Investment & Retirement Center, and may also be employees of FFFCU. These products and services are being offered through LPL or its affiliates, which are separate entities from and not affiliates of FFFCU or First Financial Investment & Retirement Center.

Securities and insurance offered through LPL or its affiliates are:

![]()

The information provided is not intended to be a substitute for specific individualized tax planning or legal advice. We suggest that you consult with a qualified tax or legal professional.

LPL Financial Representatives offer access to Trust Services through The Private Trust Company N.A., an affiliate of LPL Financial.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

CRPC conferred by College for Financial Planning.

This communication is strictly intended for individuals residing in the state(s) of CT, DE, FL, GA, MA, NJ, NY, NC, OR, PA, SC, TN and VA. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2025.